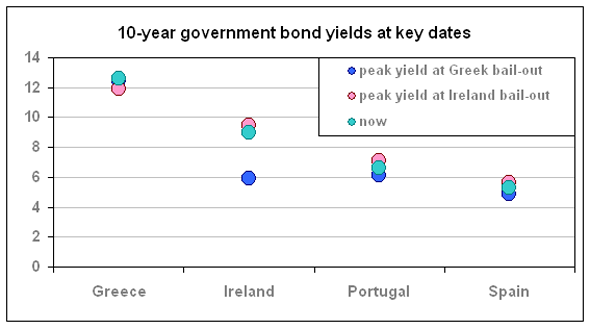

Monday, December 19, 2011

Wednesday, December 7, 2011

Sunday, December 4, 2011

Friday, December 2, 2011

Wednesday, November 16, 2011

Tuesday, November 15, 2011

Friday, November 11, 2011

Why Italy’s days in the eurozone may be numbered | The A-List | Must-read views on today’s top news stories – FT.com – FT.com

Why Italy’s days in the eurozone may be numbered | The A-List | Must-read views on today’s top news stories – FT.com – FT.com

Attempts have been made to use financial engineering to turn this small sum into €2,000bn. But the leveraged EFSF is a turkey that will not fly, because the original EFSF was already a giant collateralised debt obligation, where a bunch of dodgy, sub-triple-A sovereigns try to achieve, by miracle, a triple-A rating via bilateral guarantees. So a leveraged EFSF is a giant CDO squared that will not work and will not reduce spreads to sustainable levels. The other “turkey” concocted by the EFSF was supposed to be a special purpose vehicle where reserves of central banks become the equity tranche that allows sovereign wealth funds and the Bric countries to inject resources in a triple-A super senior tranche. Does this sound like a giant sub-prime CDO scam? Yes, it does.

Attempts have been made to use financial engineering to turn this small sum into €2,000bn. But the leveraged EFSF is a turkey that will not fly, because the original EFSF was already a giant collateralised debt obligation, where a bunch of dodgy, sub-triple-A sovereigns try to achieve, by miracle, a triple-A rating via bilateral guarantees. So a leveraged EFSF is a giant CDO squared that will not work and will not reduce spreads to sustainable levels. The other “turkey” concocted by the EFSF was supposed to be a special purpose vehicle where reserves of central banks become the equity tranche that allows sovereign wealth funds and the Bric countries to inject resources in a triple-A super senior tranche. Does this sound like a giant sub-prime CDO scam? Yes, it does.

Wednesday, November 9, 2011

Monday, November 7, 2011

Thursday, November 3, 2011

Wednesday, November 2, 2011

Monday, October 24, 2011

Saturday, October 22, 2011

Friday, October 21, 2011

Tuesday, October 18, 2011

Monday, October 17, 2011

Saturday, October 15, 2011

Tuesday, October 4, 2011

Monday, October 3, 2011

Thursday, September 29, 2011

Wednesday, September 28, 2011

Monday, September 26, 2011

Sunday, September 25, 2011

Monday, September 19, 2011

Friday, September 16, 2011

Thursday, September 8, 2011

Tuesday, September 6, 2011

Monday, August 29, 2011

Tuesday, August 23, 2011

Why the Bundesbank opposed bond purchases | Money Supply | News, data and opinions on market-moving economics from the Financial Times – FT.com

Why the Bundesbank opposed bond purchases | Money Supply | News, data and opinions on market-moving economics from the Financial Times – FT.com

Bundesbank: interest payments as a share of gross domestic product had fallen significantly for both Spain and Italy since Europe’s monetary union was launched at the beginning of the 1990s.

Bundesbank: interest payments as a share of gross domestic product had fallen significantly for both Spain and Italy since Europe’s monetary union was launched at the beginning of the 1990s.

http://www.globalpost.com/dispatch/news/regions/africa/110823/finding-gaddafis-billions

http://www.globalpost.com/dispatch/news/regions/africa/110823/finding-gaddafis-billions

Daniel Serwer, a senior fellow at the Johns Hopkins University School of Advanced International Studies and a scholar at the Middle East Institute, said Libya's new Transitional National Council could have a "very difficult" time regaining state assets.

"I can guarantee you right now someone is trying to privatize whatever assets are sitting in Libya's central bank, privatizing land, offices, and stealing computers. This is what goes on," Serwer said during a conference call Monday afternoon, hosted by the Council on Foreign Relations.

Daniel Serwer, a senior fellow at the Johns Hopkins University School of Advanced International Studies and a scholar at the Middle East Institute, said Libya's new Transitional National Council could have a "very difficult" time regaining state assets.

"I can guarantee you right now someone is trying to privatize whatever assets are sitting in Libya's central bank, privatizing land, offices, and stealing computers. This is what goes on," Serwer said during a conference call Monday afternoon, hosted by the Council on Foreign Relations.

Friday, August 12, 2011

Thursday, August 11, 2011

Wednesday, August 10, 2011

Tuesday, August 9, 2011

FT Alphaville » The distressed euro, via French (and German) CDS

FT Alphaville » The distressed euro, via French (and German) CDS

http://av.r.ftdata.co.uk/files/2011/08/Markit-DE-FR-with-SovX-bps.png

http://av.r.ftdata.co.uk/files/2011/08/Markit-DE-FR-with-SovX-bps.png

Monday, August 8, 2011

Wednesday, August 3, 2011

Sunday, July 24, 2011

Monday, July 18, 2011

Monday, July 4, 2011

Wednesday, June 29, 2011

Tuesday, June 28, 2011

Monday, June 27, 2011

Sunday, June 26, 2011

Wednesday, June 22, 2011

Tuesday, June 21, 2011

Thursday, June 16, 2011

Thursday, June 9, 2011

Thursday, March 10, 2011

Thursday, February 3, 2011

Saturday, January 29, 2011

Monday, January 24, 2011

FT: low volatiliy in energy options prompts shift to soft commodities

Energy traders usually follow gas storage data and Opec statements... low volatility due to ample supply

Sunday, January 23, 2011

Wednesday, January 12, 2011

Tuesday, January 11, 2011

FT: Basel III credit bubble regulation

...The agreement, struck last month, says that if a country decides its economy is overheated – based on the ratio of credit to gross domestic product – it can require banks within its borders to hold extra capital against potential losses.

Regulators in every other country would have to follow suit and impose a proportional surcharge on their own banks, based on the size of those institutions’ exposure to the bubble country.

Regulators in every other country would have to follow suit and impose a proportional surcharge on their own banks, based on the size of those institutions’ exposure to the bubble country.